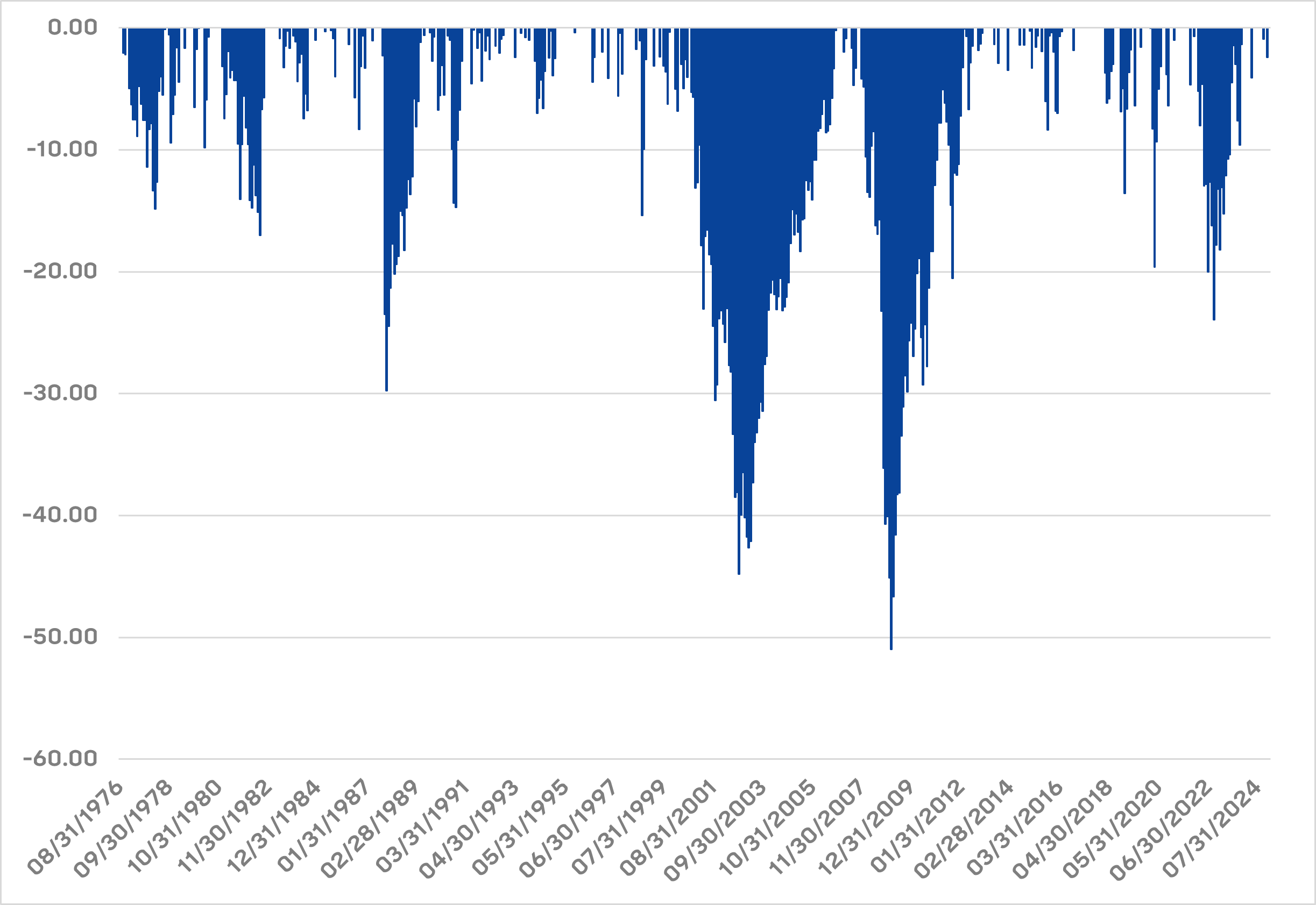

It’s every investor’s worst nightmare—putting money to work right before a massive market decline. I’ve seen this fear paralyze investors and cause them to hold way too much cash in their portfolios. I get it. It’s overwhelming—if not downright discouraging—to consider the possibility that an ill-timed investment in the stock market might immediately destroy your hard-earned wealth. For example, a long-term investor in the Vanguard 500 Index fund has faced some harrowing drawdowns. Since its August 1976 inception through February 2025, the fund has dropped 10% or more 20 times, with six of those instances culminating in bear markets (defined as a drop of 20% or greater).

% Drawdowns — Vanguard 500 Index Investor

That said, the probability of an investor picking a random day that happens to be the peak before a significant market decline is very low. The chances are between 1 in 300 and 1 in 500 when considering market declines of 10% or more, and 1 in 1,500 to 1 in 1,800 when considering exclusively 20% drops. Statistically speaking, though, some investors have experienced terrible luck regarding the timing of their investments, and it’s instructive to see how these investors have fared.

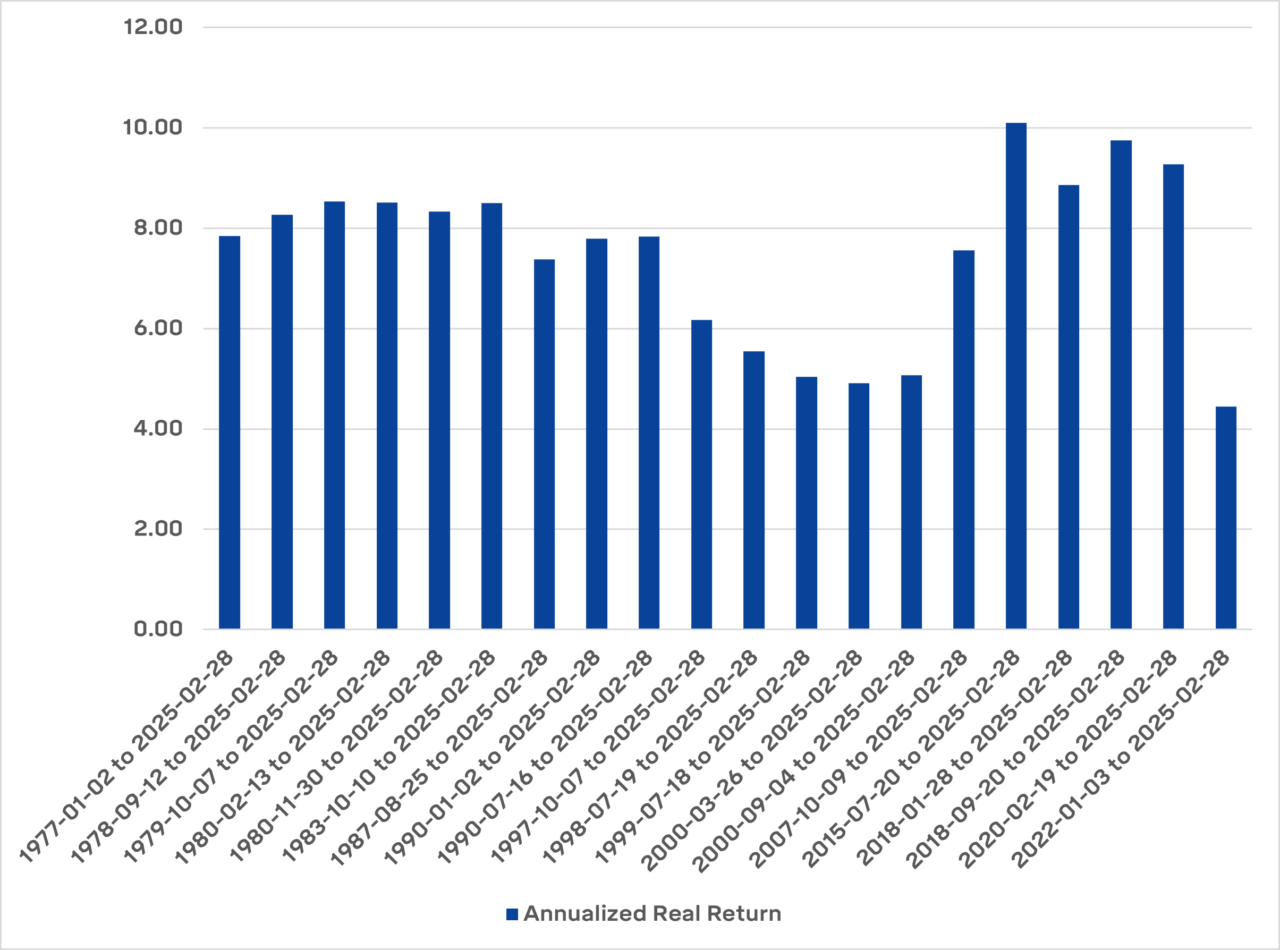

The chart below takes a closer look at the annualized returns a hypothetical investor would have earned if she invested a lump sum in the Vanguard 500 Index at various dates directly preceding the fund’s worst drawdowns since its inception—during the 70s stagflation, just before Black Monday, during the dot-com bubble, before the financial crisis, and the COVID-induced market-crash. In each bad luck scenario, a buy-and-hold investor did okay.

Investing Right Before a Market Decline

Having some of the worst investment luck imaginable has undoubtedly mattered, but not to the extent that it would have been detrimental to sensible investment goals. Every instance of misfortunate timing eventually resulted in meaningfully positive real returns through February 2025, provided the investor simply held tight. Five of the worst examples delivered between 4-6% real returns: July 19, 1998; July 18, 1999; March 26, 2000; September 4, 2000; and January 3, 2022. The first four of those occurrences happened during the dot-com era of eye-wateringly lofty valuations. In contrast, the 2022 case saw below-average real returns mostly attributable to the headwind caused by a surge in inflation and the short measurement period to earn back the losses (just the three years between 2022 and today). Even the most anvil-to-the-head or fall-off-a-cliff instances of bad-luck investing have failed to reduce a market-cap-weighted portfolio of U.S. large-caps to roadkill over time.

To be sure, caveats abound: Hindsight is 20/20; trailing return data is sensitive to its end point; an investor would have had to hold on through thick and thin, etc. Nevertheless, an investment in an S&P 500 index fund has done a more-than-sufficient job of protecting purchasing power, even if that investment was at the most inopportune time.

Even if your timing is catastrophically bad, history shows that a diversified investment in U.S. large-cap stocks still tends to reward patience. The lesson? Luck matters, but time matters more. If you stay invested and avoid panicking, your portfolio will likely recover and deliver strong, positive real returns. In investing, resilience beats perfection.